Commercial Construction in 2026: The Five Forces Reshaping Every Project in America

If you're developing, financing, or building commercial real estate anywhere in the United States right now, the ground beneath your project has shifted. The cost to build has become harder to predict. The workforce needed to build it has become harder to find. And the policies shaping both — from trade tariffs to immigration enforcement — show no sign of stabilizing anytime soon.

This isn't a cyclical downturn. The challenges reshaping commercial construction in 2026 are structural, layered, and compounding — affecting everything from a neighborhood QSR buildout to a multi-million-dollar medical campus. Understanding them isn't optional for project owners, developers, and real estate professionals. It's the price of entry for getting a project off the ground and across the finish line.

At Terrapin Construction Group, we manage commercial builds across all 50 states — from QSR and retail fit-outs to cannabis cultivation facilities and medical offices. What we're seeing in the field matches exactly what the data is showing. Here is a frank, fully sourced breakdown of what's hitting the industry hardest in 2026 — and what you can do about it.

1. Tariffs Have Sent Construction Material Costs Into a New Baseline

The single most disruptive force hitting commercial construction budgets in 2026 is federal trade policy. Steel and aluminum — the skeletal system of nearly every nonresidential building — are now subject to Section 232 tariffs of 50%. Copper, essential for every electrical and mechanical system in a commercial build, carries a 50% tariff on semi-finished derivatives. Softwood lumber sits at 10% with certain derivatives taxed at 25%. And a sweeping global tariff of 10% — affecting most international trade partners through July 2026 — is still working its way into supplier pricing at every level of the supply chain.

The results are already showing up on bid sheets and change order logs. According to Associated Builders and Contractors, nonresidential construction input prices surged at an annualized rate of 7.1% in January 2026 alone — driven by sharp increases in copper wire and cable, iron, steel, and industrial controls equipment. JLL's 2026 construction cost outlook projects that aggregate construction costs could rise roughly 8% under current tariff policy — with material-specific impacts ranging from 5% to 25% depending on the category.

Perhaps most damaging for project planning is the unpredictability. Cushman & Wakefield estimates that current tariff rates will push total CRE project costs up 4.6% relative to 2024 baselines. But the policy environment remains fluid. The 10% global tariff is scheduled to expire in July 2026. Reciprocal tariffs ranging from 15 to 40% are still in effect for most countries. Any escalation — another round of steel duties, new tariffs on electrical equipment or glass — could reprice an entire project mid-bid.

For project owners, this creates a specific and painful problem: construction contracts signed today are being built with materials priced tomorrow. S&P Global notes that uncertainty surrounding tariff policy is causing delayed investment decisions and, in some cases, project cancellations — particularly in sectors sensitive to steel and aluminum pricing like data centers, industrial facilities, and large-scale retail.

What forward-thinking owners and GCs are doing: locking in long-lead materials — structural steel, aluminum systems, copper wire, switchgear — months before they're needed. Terrapin's preconstruction services are specifically designed to front-load this kind of procurement intelligence before you're exposed. Early GC involvement during design is no longer a nice-to-have — in the current tariff environment, it is a cost-control imperative.

2. The Construction Labor Shortage Has Reached a Critical Threshold

Labor has been the construction industry's most persistent structural challenge for years. In 2026, it has become an acute crisis. The Associated General Contractors of America reports that 92% of contractors are having difficulty filling open positions. Forty-five percent of firms say labor shortages are actively causing project delays. Nearly 80% of firms report at least one delayed project in the past twelve months — and workforce gaps are the leading reason.

The numbers behind the shortage are stark. According to JLL's construction cost analysis, the industry needs approximately 500,000 additional workers above normal hiring levels in 2026 alone to meet projected demand. Nearly 40% of the skilled construction workforce is over age 45, accelerating retirement attrition faster than new entrants can replace them. Electricians, heavy equipment operators, superintendents, and project managers are commanding premium wages — and even at higher pay, positions remain open.

The trades most difficult to fill, according to AGC's workforce survey, span the full spectrum of a commercial build: electricians, carpenters, concrete workers, heavy equipment operators, and crane operators — more than 75% of firms reported trouble finding qualified candidates in each of these categories. This isn't a regional phenomenon. It's national, and it's showing up equally on a tenant improvement in Denver as it is on a ground-up retail center in Houston.

The structural drivers go beyond demographics. Decades of messaging that steered young Americans toward four-year college degrees hollowed out the pipeline for vocational and trades education. As NPR's reporting on the labor shortage makes clear, the industry had been filling this gap with immigrant labor — documented and otherwise — for over two decades. Now those labor flows are tightening for reasons that are accelerating further disruption.

3. Immigration Enforcement Is Compounding the Workforce Crisis

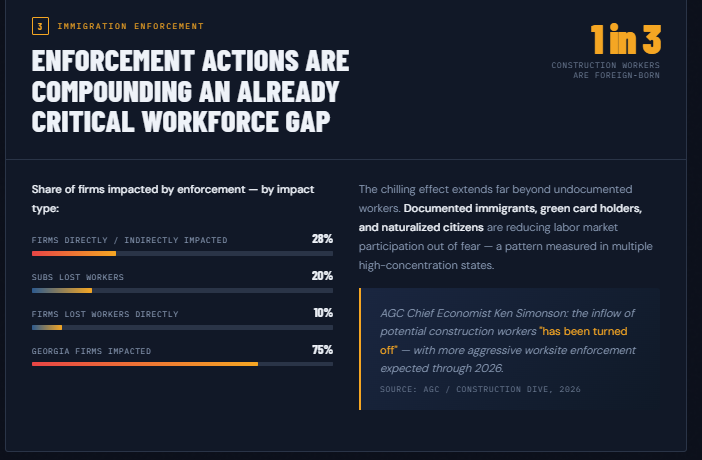

One in three construction workers in the United States is foreign-born. Immigration enforcement under the Trump administration has already begun to reshape who shows up on job sites — and the effect is accelerating as 2026 progresses.

According to the AGC's latest workforce survey, 28% of construction firms have been impacted — directly or indirectly — by immigration enforcement actions in the past six months. Ten percent of contractors reported losing workers due to actual or rumored ICE actions. Twenty percent report that their subcontractors lost workers. In Georgia, that figure reached 75% of all surveyed contractors. The impact is unevenly distributed across states, but no region is immune.

What makes this particularly difficult for the commercial construction pipeline is the chilling effect that extends beyond undocumented workers. Documented immigrants, green card holders, and even naturalized citizens are reducing their labor market participation out of fear for themselves or family members — a pattern the Urban Institute has documented in states with high construction workforce concentrations.

The American Immigration Council's analysis found that the 10 states with the highest concentration of undocumented immigrants in construction saw a 0.1% drop in construction employment during a period when other states saw a 1.9% increase — an early but measurable divergence. AGC chief economist Ken Simonson told Construction Dive that the inflow of potential construction workers "has been turned off," and that 2026 may see more aggressive worksite enforcement as ICE builds capacity.

The practical consequences for project owners: schedule risk is rising. Labor-dependent milestones — framing, concrete, MEP rough-in — are becoming harder to sequence with confidence. Working with a construction manager who has strong, verified subcontractor relationships and self-performing capacity is increasingly the difference between a project that delivers on schedule and one that doesn't.

4. The Design-Over-Budget Problem Is Getting Worse — Not Better

Here is a pattern that plays out on roughly nine out of ten commercial construction projects in the United States: an owner hires an architect, the architect designs a building, the building goes to a GC for pricing — and the GC comes back with a number that's 20 to 40% over budget. What follows is a redesign loop that eats months of schedule and hundreds of thousands of dollars in soft costs.

In 2024 and 2025, this problem was manageable if painful. In 2026, with tariff-driven material costs still moving and labor pricing tightening, a project designed without real-time construction cost input isn't just over budget — it may be unfundable. The American Institute of Architects projects commercial construction spending to increase 4.2% in 2026, but that optimism is predicated on projects being properly budgeted from the start. Projects that enter the pricing phase over-designed or under-estimated are being shelved or canceled at rates that didn't exist two years ago.

The solution isn't complicated, but it requires changing the sequence of who gets involved and when. Engaging a general contractor during precon — before schematic design is locked in — gives owners current, real-world cost data to validate design decisions against market reality. It eliminates the redesign loop entirely. Terrapin's preconstruction team works directly with ownership and design partners including 3rd Act Architecture & Consulting on specialized facility types to ensure every design decision is buildable within the owner's budget before a dollar is committed to construction documents.

The most cost-effective tool available to a commercial real estate developer today isn't a smarter architect or a cheaper GC. It's an earlier GC. Design-build delivery is one approach that structurally eliminates the gap between design intent and construction reality — by unifying those teams under a single contract from day one.

5. Interest Rates and Financing Conditions Are Still Suppressing Project Starts

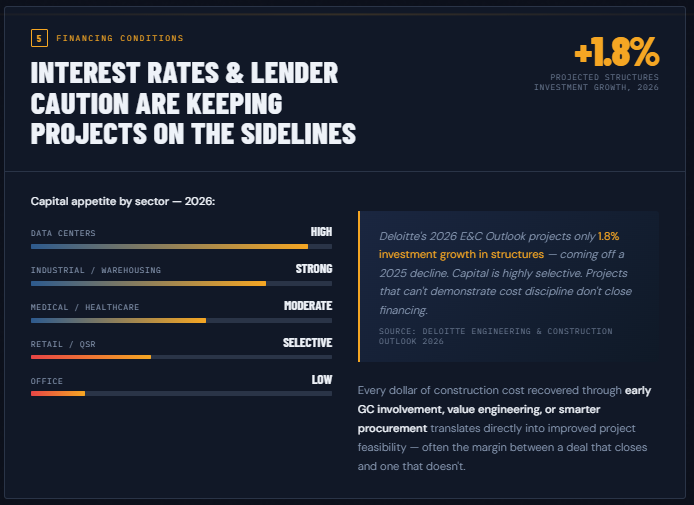

The Federal Reserve's rate cycle has eased from its peak, but financing conditions for commercial real estate construction remain meaningfully tighter than the development community was accustomed to in 2019 through 2022. Construction loan rates, equity hurdles, and lender conservatism on nonresidential projects are keeping a significant volume of deal flow on the sidelines.

According to Deloitte's 2026 Engineering and Construction Industry Outlook, interest rates, inflation, and consumer sentiment are all being closely monitored by developers of manufacturing, retail, and office properties. Investment in structures is projected to recover modestly in 2026 — roughly 1.8% growth — but this comes off a 2025 decline, and it is unevenly distributed. Data centers and energy infrastructure are attracting capital aggressively. Retail, office, and conventional commercial projects face a much higher bar.

For owners in the planning stages, this creates a direct imperative: every dollar of construction cost that can be reduced through better planning, smarter procurement, or earlier GC involvement translates directly into improved project feasibility. The difference between a project that pencils and one that doesn't often comes down to 5 to 8% of hard costs — which is precisely the range that proactive preconstruction and value engineering can recover.

Owners who are exploring value engineering for commercial facilities or who need a pre-engineered metal building solution to reduce structural costs have options that weren't as accessible before the cost environment changed. TCG's equipment procurement division also helps owners reduce carrying costs on long-lead mechanical and electrical equipment by getting it specified, ordered, and on a lead-time clock as early as possible in the design process.

What Smart Owners and Developers Are Doing Right Now

The owners and developers navigating 2026 most successfully share a handful of practices. They are engaging their GC before design is complete — ideally at schematic design or earlier. They are front-loading materials procurement for tariff-sensitive items. They are vetting their GC's subcontractor relationships directly, asking hard questions about trade coverage and self-performance capacity in a tight labor market. And they are stress-testing their project budgets against current cost data rather than pro formas built on 2023 or 2024 benchmarks.

They are also looking carefully at delivery method. Cost-plus and GMP contracts are gaining traction as owners seek more transparency into how their construction dollars are being spent in a volatile pricing environment. Understanding which delivery method fits your risk tolerance and project type is a foundational decision that shapes everything that follows.

Whether you're building a retail tenant improvement, a QSR, a medical or optometry office, or a specialized commercial facility — the 2026 commercial construction landscape rewards preparation and punishes assumptions. The teams that win are the ones that started planning earlier, structured their contracts more carefully, and chose construction partners with the bench strength to absorb market volatility without passing it entirely to the owner.

Ready to Build Smarter in 2026?

Terrapin Construction Group delivers commercial general contracting and construction management services nationwide — with offices in Denver, Houston, Albany, and Sheridan. We bring GC-level cost intelligence into the design process early, so your project doesn't get priced out of the market after you've already spent money on architecture.

If you're in planning, design, or early development on a commercial project and want a frank conversation about what it costs to build in today's environment, we'd welcome a 30-minute call.

Schedule a conversation with our team → calendly.com/will-terrapincg/30min

Sources

Associated General Contractors of America — Tariff Resource Center for Contractors

AGC — Construction Workforce Shortages Survey

Construction Dive — Tariffs Drove Construction Input Prices Up, Jan. 2026

Construction Dive — How Immigration Enforcement Will Impact Construction in 2026

Deloitte — 2026 Engineering and Construction Industry Outlook

Cushman & Wakefield — The Impact of Tariffs on CRE Construction Costs

JLL / Tax Credit Advisor — 2026 U.S. Construction Cost Outlook

S&P Global — US Tariffs: Impact on the Construction Industry

NPR — Trump's Immigration Crackdown Is Hurting the Construction Industry

Urban Institute — Mass Deportations Would Worsen Our Housing Crisis

American Immigration Council — Immigration Toll on Local Economies

Engineering News-Record — ICE Enforcement Adds to Construction's Labor Shortage Woes