What National Commercial Developers Actually Lose When the GC Relationship Breaks Down

The commercial real estate development business runs on underwriting assumptions that were made months or years before a project goes vertical. Pro formas get built, capital gets committed, lenders get brought in, and tenants or buyers get made promises. Every one of those assumptions is downstream of one fundamental question: will the building get built on budget and on schedule?

The answer, too often, is no. And when it is no, the reason is almost never the site, the market, or the asset class. It is the construction execution. According to McKinsey & Company, large construction projects on average run 80% over budget and 20 months behind schedule. That is not a rounding error. That is the difference between a project that performs and one that does not — and it is directly traceable to decisions made in how the GC relationship is structured, when the GC is engaged, and whether the accountability architecture of the project actually holds up under pressure.

At Terrapin Construction Group, we work with commercial real estate developers operating at national scale across retail, QSR, industrial, healthcare, and commercial sectors in all 50 states. This article identifies the seven most consistent pain points we see in developer-GC relationships — the ones that show up across portfolios, across markets, and across asset classes — and addresses how a properly structured national GC engagement resolves them before they cost you money.

Pain Point 1: Designs Delivered Over Budget — and the GC Who Could Have Prevented It Was Not in the Room

This is the single most consistent and expensive problem in commercial development, and it is entirely preventable. An owner hires an architect. The architect designs a building. The design goes to a GC for pricing. The number comes back 15, 20, or 30 percent over what the pro forma assumed. The project either gets redesigned — costing time, fees, and schedule — or it proceeds over budget, compressing the return.

According to the American Institute of Architects, the majority of commercial projects are delivered to a contractor for first pricing with a design that exceeds the owner's stated budget. The QSR, retail, and healthcare sectors are particularly vulnerable to this pattern because their projects appear straightforward — and architects working without real-time construction cost data routinely underestimate MEP scope, structural complexity, site work, and the cascading cost implications of late-breaking program decisions.

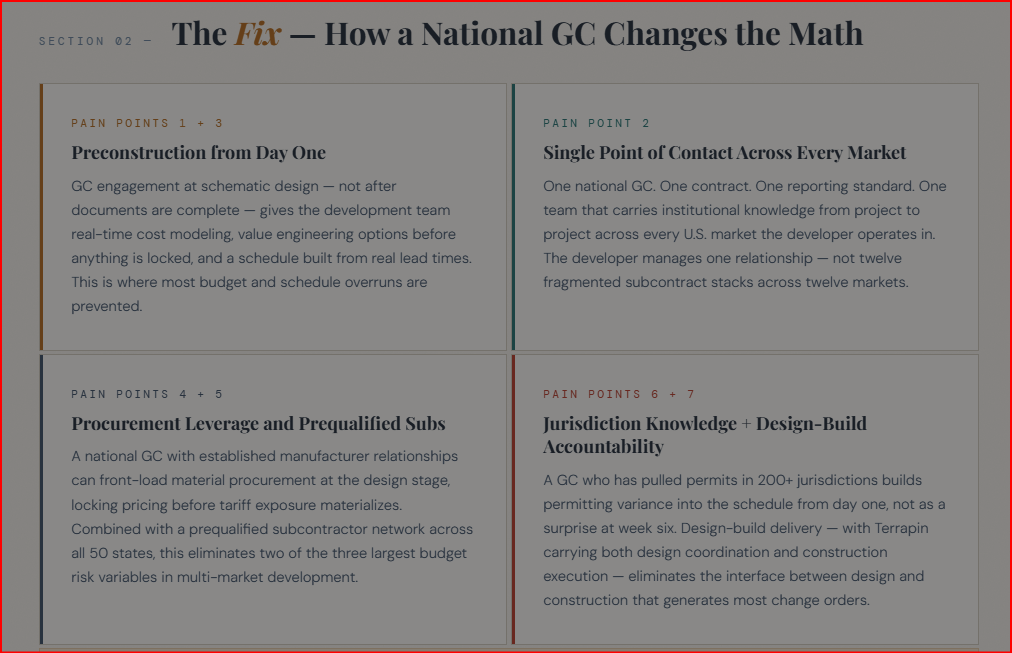

The fix is simple in principle and almost never implemented: engage the GC at schematic design, not after construction documents are complete. Terrapin's preconstruction services are specifically structured for this purpose. Owners who bring us in at the design stage get real-time cost modeling as design evolves, value engineering options before anything is locked into the documents, and constructability review that closes the gap between design intent and buildable reality. The cost of this engagement is a fraction of the cost of a single redesign cycle — and it eliminates the single most predictable budget failure in commercial development.

As Procore's construction cost overrun analysis documents, identifying risks early and managing changes responsibly before construction begins is the most reliable predictor of whether a project will stay within budget. The window for that to happen is preconstruction. Once the documents are issued for permit, the opportunity to design out cost is largely gone.

Pain Point 2: Multi-Market GC Fragmentation — Different Standards, Different Accountability, No Single Point of Contact

National developers building across multiple U.S. markets frequently solve the "who builds it" problem by hiring the local GC in each market. The logic is reasonable on the surface: local contractors know the subcontractor community, the permit offices, the inspectors, and the site conditions. What this approach sacrifices is equally significant: consistency of standards, reporting, and accountability across the portfolio.

A developer running five projects simultaneously in Dallas, Nashville, Denver, Philadelphia, and Portland is functionally managing five separate GC relationships, five different reporting formats, five different communication protocols, and five different cultures of accountability. When a problem surfaces in one market, there is no institutional knowledge transfer to the others. When a subcontractor underperforms in one market, the lesson does not benefit the next project. When budget pressure hits, each GC handles it differently — with no consistent developer-side visibility into where the exposure actually is.

The NAIOP Commercial Real Estate Development Association has documented the operational complexity that multi-market development creates, particularly around construction oversight, permitting coordination, and quality control. These are not problems of geography — they are problems of structure. A national GC with established operations across all 50 states eliminates the fragmentation. One contract. One point of contact. One set of reporting standards. One team that carries institutional knowledge from market to market and project to project.

Terrapin Construction Group's four offices — Denver, Houston, Albany, and Sheridan — are specifically positioned to serve multi-market commercial development portfolios across every major U.S. construction cost region. Our construction management structure is designed to give national developers a single organizational interface regardless of how many markets they are building in simultaneously.

Pain Point 3: Schedule Overruns That Were Preventable — and the Pro Forma Damage They Do

Schedule overruns are not random events. They are the predictable output of specific, identifiable failures in project planning and execution: incomplete permit submissions, subcontractor scheduling conflicts, material lead times that were not accounted for, structural framing tolerances that do not accommodate what the downstream trades need, and change orders that cascade across the critical path because no one caught the coordination conflict before it hit the field.

The financial consequences of schedule overruns for developers are severe and multidimensional. Construction loan interest keeps accumulating on a project that is not generating revenue. Tenant lease commencement dates that were underwritten to a specific delivery trigger either get missed — costing the developer in free rent concessions and tenant improvement delays — or get hit with a project that is not actually ready for occupancy. Lender milestones get tripped. If the delay extends long enough, lender extensions come with fees or recourse. The carrying cost of a 60-day schedule overrun on a $5 million commercial project can easily represent $50,000 to $150,000 in additional financing cost, lost revenue, and fee penalties — before accounting for the GC overhead costs that continue to run through the extended duration.

Per Bellwether Advisors' 2025 commercial construction market analysis, what previously took 2 to 4 weeks for delivery of key materials now requires 12 to 16 weeks — and project proformas relying on pre-2023 assumptions about procurement timelines have been rendered obsolete mid-construction, jeopardizing the funding that supports them.

The disciplines that prevent schedule overruns are not mysterious: accurate preliminary scheduling with real lead times built in from the start, early permit submission with complete drawing packages, front-loaded subcontractor buyout so schedule conflicts surface before they are on the critical path, and proactive procurement of long-lead items before the structural frame is even complete. Terrapin's preconstruction and construction management teams treat schedule as a deliverable — not an aspiration. The difference between a project that hits its delivery date and one that does not is almost always traceable to decisions made in the first 90 days of the project.

Pain Point 4: Material Cost Exposure Nobody Priced — and the Tariff Environment Making It Worse in 2026

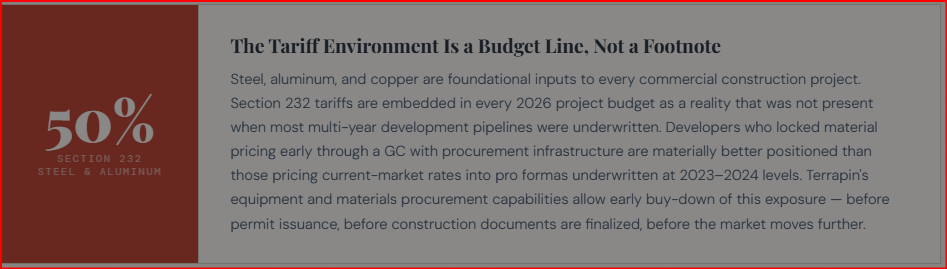

Steel, aluminum, copper, and lumber are foundational inputs to every commercial construction project. In 2026, Section 232 tariffs of 50% on steel and aluminum are embedded in every project budget as a reality that was not present when most multi-year development pipelines were underwritten. The NAIOP analysis of current tariff impacts documents how increases in import tariffs on construction inputs directly reduce developer margins — and that the impact is not uniformly distributed. Developers who locked material pricing early through GC relationships with established procurement infrastructure are materially better positioned than those who are pricing current-market steel and aluminum into projects that were underwritten at 2023 or 2024 prices.

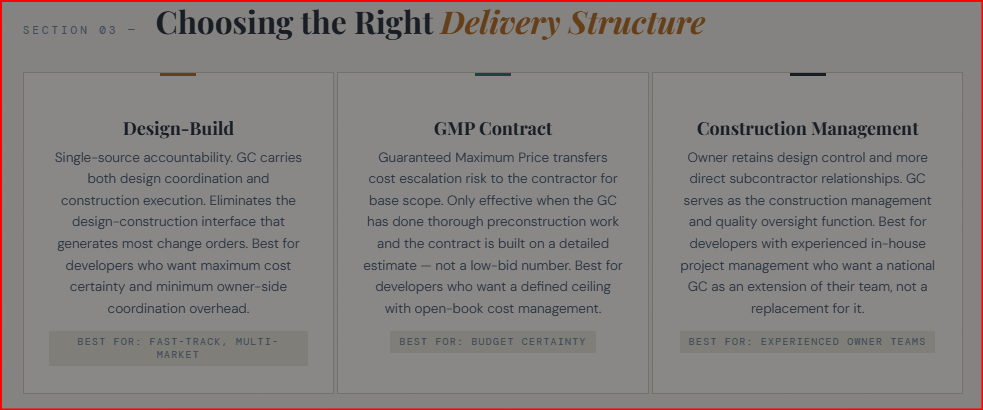

As we covered in depth in our article on commercial construction delivery methods and cost certainty, the structure of the GC contract is the primary tool available to developers to manage this exposure. A Guaranteed Maximum Price (GMP) contract — structured with a GC who has done the preconstruction work to price accurately — transfers cost escalation risk to the contractor for the base contract scope. A cost-plus contract with a GC who front-loads material procurement locks in pricing before the market moves. The developer who hands a set of completed construction documents to a GC and asks for a lump-sum bid in a tariff-volatile market is taking on cost exposure that the contract structure could eliminate.

Terrapin's equipment and materials procurement capabilities extend to early material buys on behalf of developer clients — allowing cost locking at the design stage, before permit issuance, on projects where the material specification is known with reasonable confidence. This is a tangible dollar-value service, not a theoretical one: on steel-intensive commercial projects, front-loading procurement by 60 to 90 days relative to a conventional bid-build timeline has consistently produced meaningful cost savings relative to market-rate pricing at the time of conventional GC procurement.

Pain Point 5: Subcontractor Quality Inconsistency Across Markets — the Risk You Cannot See Until It Is a Problem

One of the least discussed and most consequential risks in multi-market commercial development is subcontractor quality variance. In a developer's home market, the project team has developed relationships with subcontractors over years — they know who does good work, who hits their schedule commitments, who is financially stable enough to perform through a long project without cash flow issues, and who to avoid. In an unfamiliar market, that institutional knowledge does not exist. The default solution — lowest-bid subcontractor selection — consistently produces the highest total project cost once rework, delays, and warranty claims are factored in.

According to Procore's analysis of subcontractor management best practices, careful subcontractor prequalification — balancing cost against experience, reliability, and the ability to deliver quality within budget and schedule constraints — is one of the most reliable drivers of project cost control. A GC with a prequalified subcontractor network across all 50 states brings that institutional knowledge into every market the developer enters. The developer is not managing subcontractor risk; the GC is.

This is precisely what Terrapin's commercial general contracting operations provide to national developer clients: an established, prequalified subcontractor network across major U.S. markets, with the project track record and financial stability assessments that protect developer clients from the most common single point of failure in multi-market construction. The GC who vets the subs carries the accountability. The developer who has to manage that vetting themselves in 12 different markets is carrying a risk that a national GC relationship eliminates.

Pain Point 6: Permitting Complexity Across Jurisdictions — the Schedule Killer Nobody Budgets For

Permitting is the most consistently underestimated schedule risk in national commercial development. Developers who build in their core markets understand the permit office, the typical review cycle, the inspectors, and the political dynamics that affect approval timelines. In unfamiliar markets, that knowledge does not exist — and the variance is enormous. A commercial building permit in suburban Texas might be issued in three to four weeks. The same project in a California jurisdiction subject to CEQA environmental review or design review board approval can consume six months before a shovel goes in the ground.

The 2026 commercial real estate outlook from PBMares confirms that permitting timelines and local regulatory conditions are now among the primary site-selection considerations for national developers — particularly in markets where power availability, zoning reform, and environmental review create unpredictable approval cycles. Developers who are not pricing permitting timeline variance into their schedules are carrying exposure that routinely materializes as 60- to 180-day schedule slippage before construction begins.

An experienced national GC who has pulled permits in dozens of jurisdictions across all 50 states brings a fundamentally different level of jurisdiction-specific knowledge than a local contractor who has operated in a single market. At Terrapin, we have built relationships with plan examiners, permit offices, and inspection authorities across every major U.S. construction market. When we identify a jurisdiction with an aggressive review cycle, we build that into the project schedule from day one — not as a surprise at week six of what was supposed to be a four-week permit cycle. Our owners' representative services extend this permitting oversight to developer clients who want a single point of accountability for the full pre-construction process from site control through permit issuance.

Pain Point 7: The Change Order Culture — and How to Negotiate Your Way Out of It Before It Starts

Change orders are where developer-GC relationships most visibly deteriorate — and where the structural weaknesses of a poorly constructed engagement most clearly reveal themselves. A GC who was selected primarily on low bid, working from incomplete construction documents, with an owner who made scope decisions during construction that were not captured in the original contract, is a change order factory. The developer who has been through this cycle understands it intuitively. The developer who has not yet experienced it at scale is about to.

The conditions that produce excessive change orders are not mysterious: incomplete design documentation at the time of GC engagement, owner scope decisions made during construction without formal change control, value engineering decisions that shift risk between parties without explicit agreement, and subcontractor coordination gaps that create field conflicts requiring resolution on the fly. According to VERTEX Engineering's analysis of construction management structures, unclear authority and scope gaps between design and construction teams are among the most consistent sources of project failure — and the legal disputes that follow.

The structural solutions are available and proven. A design-build delivery model — where Terrapin carries both the design coordination and construction execution under a single contract — eliminates the interface between design and construction that generates most change orders. When the GC is responsible for both the design documents and the construction execution, the incentive to generate change orders from design gaps disappears. Alternatively, a properly structured GMP contract with thorough preconstruction scope development locks the change order scope to genuine owner-directed additions, not contractor-captured ambiguity in the original documents.

The Planyard GMP contract guide confirms this directly: a GMP is most effective when a highly detailed cost estimate is developed in the preconstruction phase, with explicit contingency scope and a shared understanding of risk allocation between owner and contractor before construction begins. That pre-construction investment is precisely the discipline that eliminates the change order dynamic — and it is only possible if the GC is engaged early enough to do the work.

What a Better-Structured National GC Engagement Actually Looks Like

The seven pain points above are not independent problems with independent solutions. They are symptoms of a single structural issue: the GC is brought in too late, is selected on price rather than alignment, and is not given the accountability architecture to perform against the developer's actual goals. Fixing the structure of the engagement resolves all seven simultaneously.

For national commercial developers building across multiple markets, the highest-value version of a GC relationship looks like this: the GC is engaged at schematic design, before the design has a chance to drift away from the budget. The GC conducts preconstruction cost modeling and constructability review in parallel with design development, so the first full-document estimate reflects buildable reality. Material procurement begins at the permit submittal stage, locking pricing before the construction market moves. Subcontractor prequalification happens through the GC's established network in each market, not through a cold bid process in an unfamiliar subcontractor community. The schedule is built by the GC from real lead times and real subcontractor availability, not optimistic assumptions. The contract structure — whether GMP, design-build, or construction management — is selected based on where the risk actually sits and who is best positioned to manage it.

This is not a theoretical model. It is the approach that Terrapin Construction Group brings to national developer relationships across preconstruction, commercial general contracting, construction management, design-build delivery, and owners' representation. Our project experience spans QSR, retail, healthcare, commercial, cannabis cultivation, and industrial sectors — and our four-office footprint serves developer clients from single-site engagements through multi-project portfolio relationships across all 50 states.

The current market environment — with $1.8 trillion in commercial real estate debt maturing in 2026 per NAIOP, ongoing tariff exposure on construction materials, and a Colliers forecast of 15 to 20 percent recovery in transaction volume as institutional capital re-enters the market — makes construction execution quality more consequential than it has been at any point in the past decade. Developers who get the GC relationship right in 2026 have a structural advantage. Those who replicate the fragmented, late-engagement, low-bid model that has produced the industry's average outcomes will continue producing those outcomes.

Ready to Talk About How a National GC Relationship Actually Works?

Terrapin Construction Group builds commercial projects for national developers across all 50 states. If you are managing a multi-market development pipeline and want a direct conversation about what a differently structured GC relationship would mean for your budget certainty, schedule performance, and portfolio risk, we would welcome that conversation.

Schedule a 30-minute conversation → calendly.com/will-terrapincg/30min

Related reading from Terrapin Construction Group:

Commercial Construction Delivery Methods: Cost-Plus vs. GMP (2026)

Average Cost to Build a QSR Restaurant in the USA

The Hospital Construction Boom in 2026

How Many SF of IMP Panels Will Be Installed in the USA in 2026?

Sources

McKinsey & Company — The Construction Productivity Imperative

NAIOP — Ten Challenges Facing Commercial Real Estate in 2025

Procore — Mitigating Cost Overruns in Construction

Bellwether Advisors / Bonadio Group — State of the 2025 Commercial Real Estate Market

VERTEX Engineering — Understanding General Contractors & Construction Managers

Planyard — GMP Contract in Construction: A Comprehensive Guide

PBMares — Commercial Real Estate Outlook for 2026

Newmark — U.S. Commercial Real Estate in 2026: A Sector-by-Sector Outlook

CNBC / Diana Olick — What to Expect for Commercial Real Estate in 2026

JPMorgan — 2026 Commercial Real Estate Trends

American Institute of Architects

-

The most common GC failures are late subcontractor coordination, budget estimates that lack real market data, poor communication at project transitions, and inadequate pre-construction involvement.

-

Overruns most often occur when GCs provide budgets without current subcontractor pricing, when design changes occur after GMP is set, or when long-lead equipment isn't procured early enough.

-

Look for GCs with verifiable national subcontractor networks, preconstruction capabilities, transparent open-book budgeting, and a track record in your specific asset class and target markets.

-

Engaging a GC during schematic design allows real-time cost feedback, value engineering, early subcontractor commitments, and procurement of long-lead items — all of which reduce change orders and schedule risk.