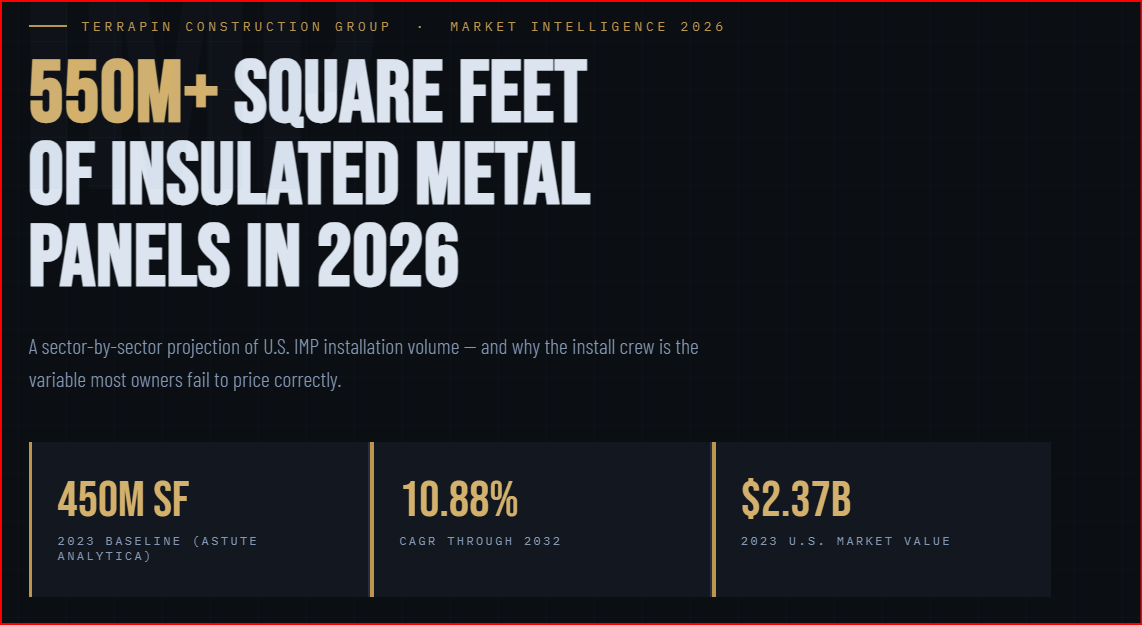

How Many Square Feet of Insulated Metal Panels Will Be Installed in the USA in 2026? A Sector-by-Sector Projection

Insulated metal panels, IMPs, are everywhere in commercial construction right now. Walk a construction site for a distribution center, a cold storage facility, a data center, a hospital wing, or a food processing plant, and there is a strong probability you are looking at IMPs on the wall or roof. They have become the building envelope solution of choice across the most active sectors of U.S. commercial real estate development because they deliver thermal performance, structural efficiency, air and moisture control, and installation speed in a single product system. The question is: how big is the 2026 market, and which sectors are driving it?

According to market research from Astute Analytica, approximately 450 million square feet of insulated metal panels were sold in the U.S. in 2023, with the market valued at $2.37 billion. Projecting forward at the sector's compound annual growth rate of 10.88% through the 2024-to-2032 forecast period, the U.S. market is on track to see more than 550 million square feet of IMP installed in 2026 — a figure that will be distributed unevenly across sectors, with industrial, cold storage, and commercial applications leading the way.

At Terrapin Construction Group, we build commercial and industrial projects across all 50 states, and IMP installation is a core competency on a significant share of our project portfolio. This article breaks down where those square footage numbers are going in 2026 by sector, what is driving demand in each category, and why the install team is the most underestimated variable in an IMP project's success.

The 2026 IMP Market Baseline: What the Numbers Tell Us

The U.S. IMP market has been growing at roughly 10-11% annually, driven by a convergence of factors that show no sign of reversing. Energy codes are tightening across more than 30 states, requiring higher continuous insulation performance. The Infrastructure Investment and Jobs Act's $1.2 trillion commitment is putting upward pressure on industrial and institutional construction spending. E-commerce and cold chain logistics are generating sustained demand for new warehouse and refrigerated storage space. And across the technology, healthcare, and manufacturing sectors, new build activity is running at levels that make 2026 a strong year for IMP demand across the board.

Applying the 10.88% CAGR from the 2023 baseline of 450 million square feet, projected U.S. IMP installations for 2026 land in the range of 550 to 570 million square feet — with the upper end reflecting accelerating adoption in cold storage and data center construction. The Research and Markets IMP report projects the overall U.S. market to reach $5.98 billion by 2032, with commercial and industrial end users commanding over 51% of that demand — a dominance that is reflected in the sector-by-sector breakdown below.

The South leads U.S. IMP consumption with a 31.7% regional market share, driven by rapid urbanization, high commercial construction volume, and active industrial development in Texas, Florida, Georgia, Tennessee, and the Carolinas. Terrapin's Houston and Denver offices are actively building IMP-specified projects across the South and Mountain West, where both the demand volume and the construction cost environment make IMP systems a particularly compelling choice.

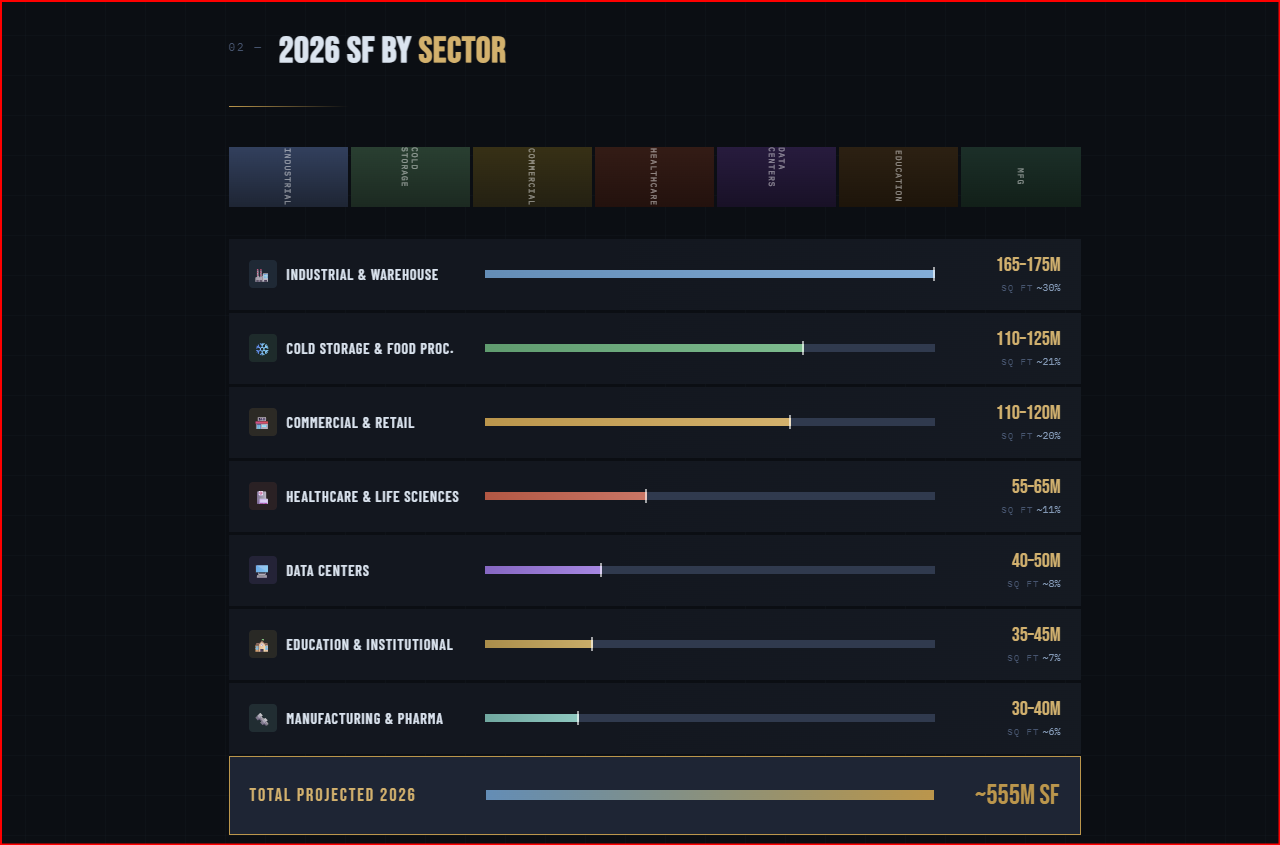

Projected 2026 IMP Installation by Sector

The following sector-by-sector breakdown is based on 2023 market share data from multiple industry research sources, projected forward to 2026 using sector-specific growth rates. Figures represent estimated square footage of IMP wall and roof panel installations across new construction and retrofit projects in the continental United States.

Industrial and Warehouse: ~165 to 175 Million Square Feet

Industrial and warehouse construction is the largest single sector for IMP installation in the U.S., accounting for roughly 30% of total square footage. The National Association of Industrial and Office Properties (NAIOP) reports that the U.S. added 1.2 billion square feet of industrial space in 2023 alone. Not all of that is IMP-clad, but the share continues to grow as developers and contractors recognize the installation speed, thermal performance, and total cost-in-place advantages of IMP systems over tilt-up concrete and conventional metal stud assemblies.

E-commerce fulfillment, last-mile logistics, manufacturing, and flex industrial are all active subsectors driving this volume. Metl-Span — one of the leading IMP manufacturers in North America — notes that the warehouse sector alone is projected to absorb hundreds of millions of square feet of new industrial space over the next several years, with IMP systems increasingly specified for their all-weather installation capability and ability to compress construction timelines in a market where speed to occupancy is a direct economic driver.

For commercial general contractors operating in this sector, IMP installation efficiency is a competitive differentiator. A four-man crew working a standard shift can install up to 5,000 square feet of IMP panels on an industrial project, per Metal Construction Association benchmarks — but only when the structural frame is properly aligned, the panels are correctly stored and sequenced, and the crew has the experience to execute without rework.

Cold Storage and Food Processing: ~110 to 125 Million Square Feet

Cold storage is one of the most structurally IMP-dependent sectors in U.S. construction. IMPs are not merely preferred for refrigerated facilities — they are functionally essential. The air-tightness, thermal performance (with R-values reaching as high as 72 in cold storage applications), and hygienic surface characteristics of IMP systems make them the building envelope standard for refrigerated warehouses, blast freezers, food processing facilities, and pharmaceutical cold chain storage.

The U.S. witnessed the construction of more than 3,000 new cold storage facilities in 2023, and demand has continued to accelerate as online grocery, pharmaceutical cold chain requirements, and aging cold storage inventory create sustained development pressure. NAIOP's 2023 analysis of IMPs in cold storage confirms that IMP wall systems can deliver installed costs 25% lower than precast insulated concrete walls in the U.S. — a meaningful advantage in a sector where the building envelope is the single largest line item in the construction budget.

Key IMP manufacturers serving this sector include Kingspan Insulated Panels, KPS Global, and Metl-Span, each offering panels designed specifically for the vapor control, sanitation, and thermal demands of refrigerated environments.

General Commercial and Retail: ~110 to 120 Million Square Feet

The broad commercial and retail category — which encompasses QSR restaurants, office buildings, mixed-use retail, car dealerships, automotive service, and general commercial — represents a large and growing share of the IMP market as developers and architects increasingly specify these systems for exterior wall applications. The combination of aesthetic flexibility, energy code compliance, and fast installation has made IMP systems a viable alternative to conventional EIFS and masonry assemblies on a wide range of commercial building types.

In 2023, more than 50 million square feet of IMPs were installed in commercial buildings. Projecting that figure forward at the commercial sector growth rate puts 2026 installations in the 110-to-120-million-square-foot range for this category. Centria and ATAS International are among the manufacturers offering architectural IMP product lines specifically designed for commercial and retail applications where facade aesthetics and design flexibility are as important as thermal performance.

Terrapin's commercial construction teams specify and install IMP systems on retail, QSR, and mixed-use commercial projects across multiple U.S. markets. Coordinating panel sequencing with MEP rough-in through integrated procurement partners like 9BA MEP is a core part of how we compress timelines on commercial IMP projects without sacrificing envelope performance.

Healthcare and Life Sciences: ~55 to 65 Million Square Feet

Healthcare construction is one of the fastest-growing IMP sectors. The U.S. is in the middle of a significant hospital and healthcare facility expansion cycle, driven by aging infrastructure, population growth in Sun Belt markets, and a post-pandemic recalibration of healthcare delivery that is pushing development into outpatient facilities, medical office buildings, surgical centers, and specialty clinics. As we covered in depth in our article on the U.S. hospital construction boom, capital spending on healthcare facilities has reached unprecedented levels.

IMP systems are particularly well-suited to healthcare applications because of their cleanability, air tightness, moisture resistance, and ability to meet stringent infection control requirements. The healthcare sector, which added more than 400 new facilities in 2023 using IMP-specified building envelopes, is projected to account for approximately 55 to 65 million square feet of IMP installation in 2026.

All Weather Insulated Panels introduced two new mineral wool panels in late 2023 specifically designed to meet fire-rated assembly requirements in healthcare and institutional construction — an example of how manufacturers are actively expanding their healthcare product lines to meet this growing sector demand.

Data Centers: ~40 to 50 Million Square Feet

Data center construction is the most explosively growing subsector for IMP demand heading into 2026. The technology industry opened more than 150 new campuses in the most recent tracking year, and the AI infrastructure build-out — which requires massive power density, precise thermal management, and fast construction schedules — is driving a level of data center development activity that the construction industry has not seen before. IMP systems are well-suited to data center construction for many of the same reasons they excel in cold storage: superior thermal performance, airtight envelope construction, and compressed installation timelines.

Projected 2026 data center IMP installations of 40 to 50 million square feet likely understate the actual market if current AI infrastructure investment levels are sustained. The CBRE U.S. data center outlook documents the scale of this buildout. For contractors managing data center IMP installations, the tolerance requirements are tighter and the schedule stakes are higher than in conventional industrial projects — which is precisely why owner experience and crew quality matter most in this sector.

Educational and Institutional: ~35 to 45 Million Square Feet

Schools, universities, government facilities, and institutional buildings collectively represent a significant and stable IMP demand base. Energy code compliance requirements in institutional construction — particularly in states that have adopted the most recent ASHRAE 90.1 continuous insulation provisions — make IMP systems an increasingly standard specification for new K-12 and higher education facilities. Sports complexes, gymnasiums, and large assembly occupancies are particularly common IMP applications in this sector, where the combination of structural span capacity and envelope performance creates a compelling case versus conventional construction.

Manufacturers including MBCI and Green Span Profiles offer product lines specifically engineered for educational and institutional applications, with fire-rated assembly options and low-embodied-carbon configurations designed to align with institutional sustainability mandates.

Residential and Light Commercial: ~35 to 45 Million Square Feet

The residential sector accounted for approximately 35 million square feet of IMP usage in 2023, driven by government-backed energy efficiency initiatives and a growing segment of custom residential and multifamily developers incorporating IMP systems for superior thermal performance and reduced operational energy costs. While residential remains a smaller share of total IMP square footage than institutional or industrial applications, it is growing faster on a percentage basis as energy codes tighten and consumer awareness of IMP performance advantages increases.

Manufacturing and Food Processing: ~30 to 40 Million Square Feet

Domestic manufacturing is experiencing a structural resurgence — reshoring driven by tariff policy, the CHIPS Act, and supply chain recalibration following the pandemic years has created a wave of new manufacturing facility construction across the U.S. Food processing plants, pharmaceutical manufacturing facilities, clean rooms, and general manufacturing buildings are all active IMP users. The hygienic surfaces, moisture resistance, and thermal performance of IMP systems are particularly well-aligned with food processing and pharmaceutical manufacturing environments where sanitation and contamination control are regulatory requirements.

Nucor Building Systems — which completed the acquisition of Cornerstone Building's IMP business in 2021 for approximately $1 billion — is one of the major manufacturers serving this sector, with product lines designed for the load-bearing and span requirements common in manufacturing facility construction.

The Variable Nobody Puts in the Budget: Install Team Quality

Here is the thing that the market size projections and sector breakdowns do not capture: a poorly installed IMP system does not deliver on anything the spec promised. The thermal performance disappears. The air tightness fails. The building envelope that was supposed to reduce energy costs by 25 to 40 percent becomes a liability. And the cost of fixing it — when it can be fixed — often exceeds what it would have cost to hire the right crew the first time.

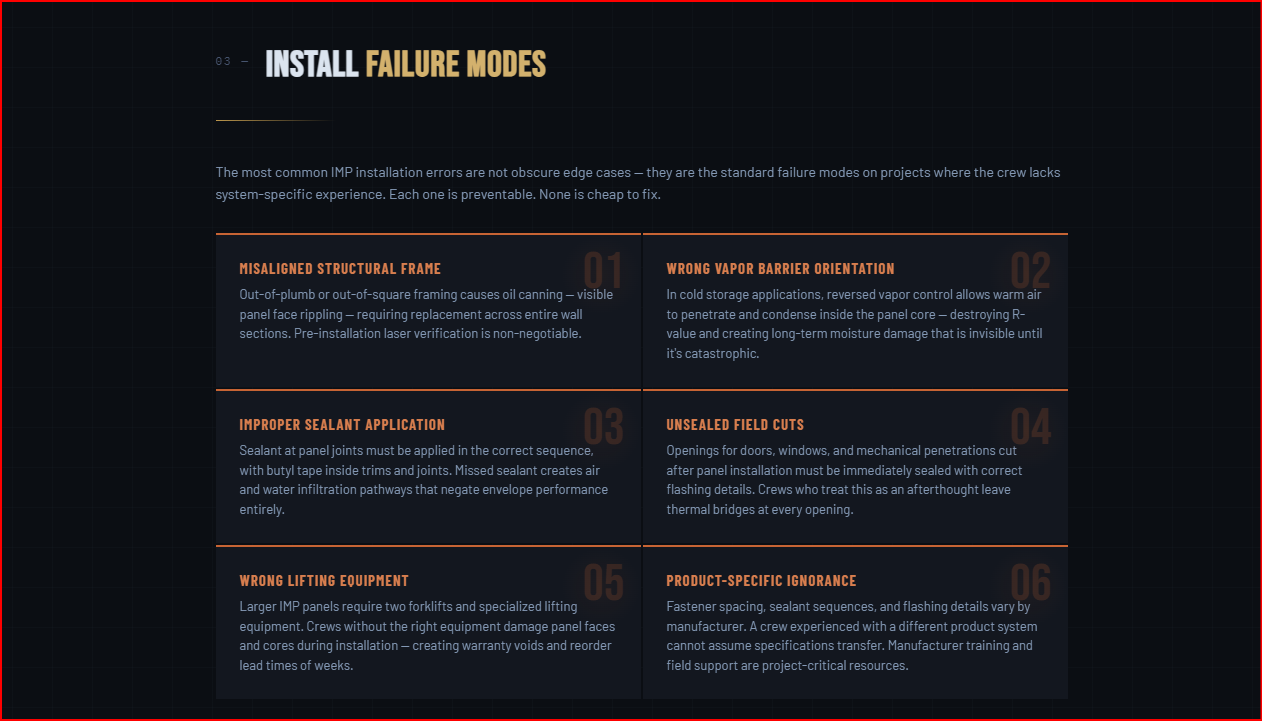

IMP installation looks simple from a distance. The panels are prefabricated and dimensionally precise. The connection system is engineered. But as Metal Construction News has documented in detail, the most common installation mistakes — misaligned structural framing, incorrect vapor barrier orientation, improper sealant application, field cutting without sealing, and using the wrong lifting equipment — are not obscure edge cases. They are the standard failure modes that show up on projects where the install crew is inexperienced, unfamiliar with the specific product system, or operating without manufacturer-level field support.

The consequences are real and expensive. Misaligned framing causes oil canning — visible rippling of the panel face — which can require panel replacement across entire wall sections. Incorrect vapor barrier placement in a cold storage application means warm, moist air penetrating the panel core, condensing inside the insulation, and destroying the R-value that justified the specification in the first place. Improper sealant application at panel joints creates air and water infiltration pathways that negate the building envelope's performance. In extreme cases, a systemically misaligned installation can cause structural failure of the panel system and require complete reinstallation — a scenario that carries not just the cost of new product and labor, but the full carrying cost of a project pushed months off schedule.

As Metl-Span puts it directly in their own technical guidance: a systemic misalignment during installation can lead to total structural failure of the panel system and require new product and a second installation. The result is cost overruns, a breakdown of trust with the building owner, and a major interruption of the completion timeline.

MBCI's installation guidance reinforces the same point from a different angle: potential consequences span from minor aesthetic headaches to extremely costly errors, including leaks and structural issues. The simplicity of IMP installation is a feature only when it is executed correctly. When it is not, it is a liability.

Why Nationwide, Experienced IMP Installation Crews Are Worth Paying For

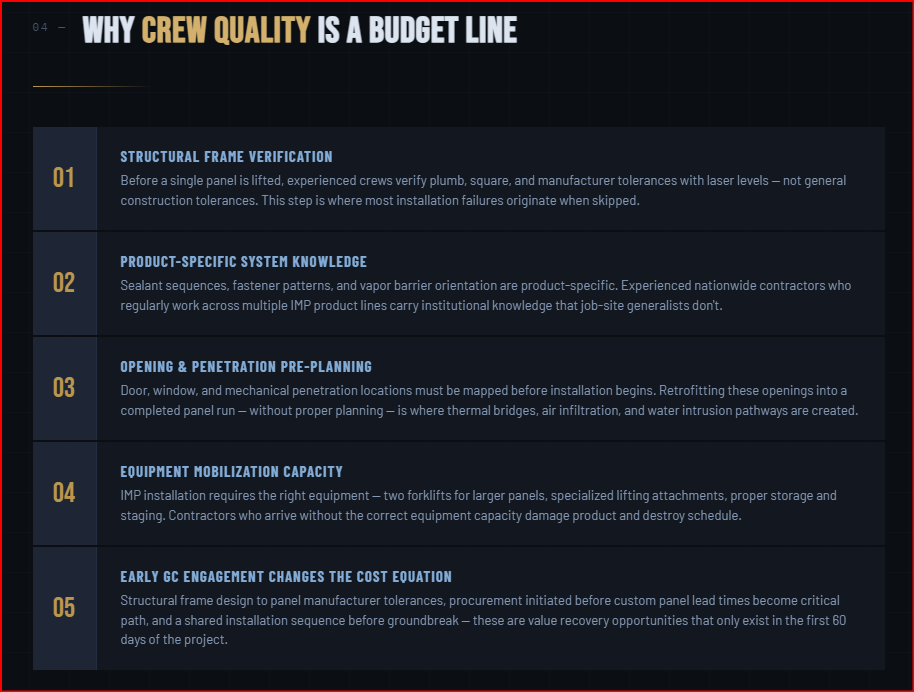

The case for working with an experienced, nationwide commercial contractor on IMP-specified projects is not a theoretical one. It comes down to five concrete factors that affect project cost, schedule, and envelope performance.

Structural frame coordination is where most IMP failures originate. Before a single panel is lifted, the structural steel must be verified for plumb, square, and compliance with the panel manufacturer's tolerances. An experienced installation team arrives with laser levels and knows how to read structural alignment against manufacturer specifications — not just general construction tolerances. This pre-installation verification step is skipped or rushed on projects where the crew is unfamiliar with IMP systems, and the consequences cascade through every subsequent panel.

Product-specific knowledge matters more than general metal panel experience. An experienced crew that installed a different manufacturer's product system on their last three jobs cannot assume that the sealant sequence, fastener spacing, vapor barrier orientation, and flashing details are the same on this project. IMP manufacturers publish detailed installation manuals, and crew familiarity with the specific product being installed is a meaningful risk variable. Experienced nationwide contractors who regularly work with multiple IMP product lines — and who maintain relationships with manufacturer technical service teams — carry a different level of institutional knowledge than crews for whom IMP installation is an occasional side of their workload.

Opening and penetration planning cannot be retrofitted after the fact. One of the most common and costly IMP installation errors occurs when crews install a continuous panel run and then cut openings for doors, windows, and mechanical penetrations without proper pre-planning. IMP panel edges exposed by field cutting must be sealed immediately and correctly — with the right flashing details, head and sill flashings, and butyl sealant applied inside trims and joints. Crews who treat this as a detail to figure out later leave thermal bridges, air infiltration pathways, and water intrusion points at every opening in the building envelope.

Equipment availability is a real constraint on IMP project logistics. Larger IMP panels require two forklifts for unloading and specialized lifting equipment during installation. A crew that arrives on a job site without the correct lifting capacity creates a cascade of problems: panels are man-handled into position in ways that damage the metal face or core, installation slows to a fraction of its possible pace, and product damage requires reorders with lead times that can push project completion dates by weeks or months. Experienced nationwide contractors have the equipment infrastructure to mobilize correctly for IMP installation scope.

Early GC engagement changes the IMP cost equation. This is the same principle that applies across every category of commercial construction: owners who engage their general contractor at the design stage recover value that owners who bring the GC in after design is complete never get back. On IMP-specified projects, early GC engagement means the structural frame can be designed to panel manufacturer tolerances from the start, procurement can be initiated early enough to account for custom panel lead times, and the project team has a shared understanding of the installation sequence before the first shovel goes in the ground.

Terrapin's preconstruction services specifically address this gap. Owners and developers who engage TCG at the schematic design stage get IMP-specific constructability review, real-time product pricing from established manufacturer relationships, and a procurement strategy that protects against mid-project schedule risk. On design-build projects, we can carry the IMP specification through design and into procurement as a single coordinated workflow rather than a handoff between teams who may have never discussed the product system together.

Pre-Engineered Metal Buildings and IMP: A Natural Pairing

A significant share of the 2026 IMP installation volume will occur on pre-engineered metal building (PEMB) projects. The structural geometry of pre-engineered metal buildings — with their engineered primary and secondary framing systems designed to defined tolerances — is highly compatible with IMP installation requirements. When the PEMB manufacturer and the IMP manufacturer are coordinating specifications, the structural alignment that IMP installation depends on is more reliably achieved. When they are not coordinating — or when the GC is managing the interface between the PEMB erector and the IMP installer without that coordination having happened upstream — the risk of framing-to-panel tolerance conflicts increases materially.

TCG's experience with PEMB-plus-IMP projects across the industrial, commercial, and cold storage sectors has informed a clear process: the PEMB scope and the IMP scope need to be managed as a single coordinated system, not as two separate subcontractor relationships. Our construction management approach treats the building envelope as a system-level deliverable, not a collection of separate trade scopes.

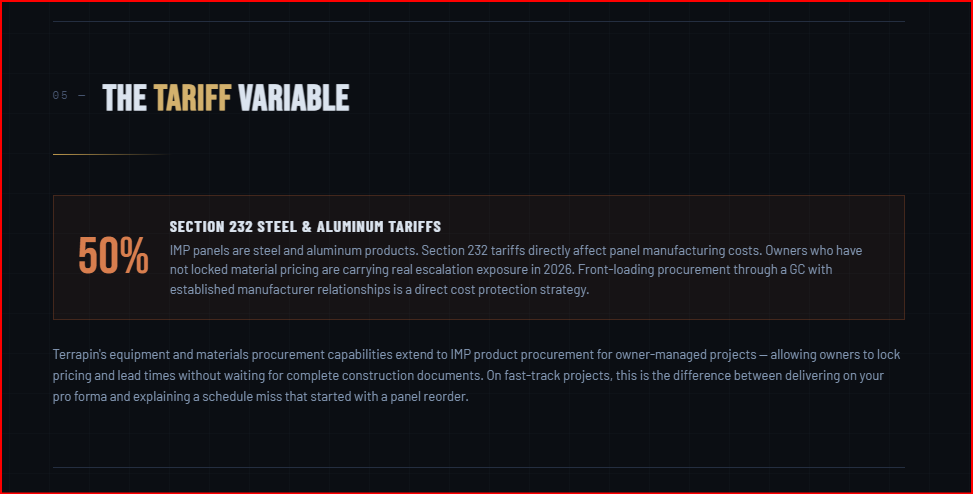

What Tariffs Mean for IMP Procurement in 2026

IMP panels are steel and aluminum products. Section 232 tariffs of 50% on steel and aluminum — the same tariff environment we covered in detail in our piece on commercial construction delivery methods — directly affect IMP manufacturing costs and, by extension, panel pricing for 2026 projects. Owners who are planning IMP-specified projects and have not yet locked material pricing are carrying real escalation exposure. The contractors and owners who have established procurement relationships with manufacturers — and who are front-loading material buys at the design stage rather than waiting until construction documents are complete — are consistently coming in better on material cost versus late-procuring projects in the same market.

TCG's equipment and materials procurement capabilities extend to IMP product procurement for owner-managed projects, allowing owners to lock pricing and lead times without waiting for a full GC engagement. This is particularly valuable on fast-track projects where design may not be complete but the project team knows with reasonable certainty which IMP product system will be specified.

Planning a Project That Includes IMP Installation? Start the Right Conversation.

The 550-plus million square feet of IMP that will be installed across U.S. commercial and industrial projects in 2026 will vary enormously in quality of outcome. The panel specification matters. The manufacturer matters. And the install team matters as much as either of those variables. Owners and developers who treat IMP installation as a commodity procurement decision are the same owners and developers who end up with oil canning, air infiltration, vapor issues, and warranty claims.

Terrapin Construction Group provides commercial general contracting, construction management, design-build delivery, and preconstruction services on IMP-specified commercial and industrial projects nationwide. If you are planning a project with a significant IMP scope, we would welcome a direct conversation about current panel pricing, installation sequencing, and how to structure the GC relationship to protect the envelope performance you are specifying.

Schedule a conversation → calendly.com/will-terrapincg/30min

Related reading from Terrapin Construction Group:

The Hospital Construction Boom in 2026

Commercial Construction Delivery Methods: Cost-Plus vs. GMP

Average Cost to Build a QSR Restaurant in the USA

Pre-Engineered Metal Buildings

Sources

Astute Analytica — U.S. Insulated Metal Panels Market Report, 2024

Research and Markets — USA Insulated Metal Panels Market Forecast 2024–2032

GlobeNewsWire — U.S. IMP Market to Generate Over $5.98 Billion by 2032

NAIOP — The Benefits of Insulated Metal Panels for Cold Storage Facilities

Metal Construction News — Five IMP Installation Mistakes

Metal Construction News — Common IMP Roof Installation Mistakes

Metl-Span — Take Five: IMP Installation Mistakes and How to Avoid Them

MBCI — How to Avoid Common IMP Installation Mistakes

Green Span Profiles — Mastering IMPs: A Guide to Sidestepping Common Pitfalls

Metal Construction Association — Selection Guide for Insulated Metal Panels

Verified Market Reports — Industrial Insulated Metal Panel Market

Kingspan Insulated Panels North America